‘Big four’ accounting firm KPMG has just asserted that cryptocurrency assets, like Bitcoin, are simply not ready to be classified as real currencies – and that using Bitcoin as a store of value is a “fool’s errand.”

In a new report , KPMG details the challenges facing the cryptocurrency industry, as it seeks adoption by the world’s largest financial institutions.

Ultimately, KPMG posits that if cryptocurrency related assets have any hopes of truly flourishing, they simply must undergo what it calls ‘ institutionalization .’

The firm defines institutionalization as the at-scale participation in the cryptocurrency market of banks, broker dealers, exchanges, payment providers, fintech companies, and other entities in the global financial services ecosystem.

“We believe this is a necessary next step for crypto to create trust and scale,” KPMG declares.

Of course, it is hardly surprising that KPMG – a company which generated $26 billion in revenue in 2017 – would hold this view. But do its arguments hold any water? Let’s dig into the report.

KPMG says Bitcoin is not a currency – yet

According to KPMG chief economist Constance Hunter, in order for a cryptocurrencies like Bitcoin to be candidates for institutionalization , they must first meet the traditional definition of a currency.

For that, a cryptocurrency asset must meet three criteria: it can be used as a unit of account, a store of value, and a unit of exchange.

The first test is easy, as cryptocurrencies are made up of identical, yet individual units of account, meant to be measured as such. For example, there are 21 million Bitcoin to ever exist – and you can account for every single one using the blockchain.

Although, as a store of value, Hunter considers cryptocurrencies to be far too unstable, especially when mapped to traditional functions of finance like borrowing.

“Consider for a moment extending a person or entity a loan in a cryptocurrency,” writes Hunter. “The value is too unstable at the moment to be assured repayment. Under these conditions, neither lenders nor borrowers would be willing to take the risk of transacting in cryptocurrencies.”

To Hunter, the act of borrowing or lending in a cryptocurrency like Bitcoin (one that risks significant devaluation) would be a “fool’s errand.” This makes cryptocurrency assets, in their current form, simply too volatile to be considered a legitimate store of value, or even an effective method of exchange.

“In order to be a medium of exchange, a crypto must be a store of value. In order to be a store of value, the speculative nature of crypto must dissipate,” Hunter explains. “Until at least one crypto meets all three criteria, they cannot be considered full currencies.”

Friction is how currencies become real

Cryptocurrency assets usually aspire to be usable currencies within the general economy, and to certain extent, Bitcoin has achieved that already.

Despite the current rates of adoption, Hunter claims that currencies only become legitimate when they find “friction” to reduce within the world economy, a fancy finance term for a solid use-case.

For example, when the Euro was first introduced within the European Union immediately simplified trade between members.

Similarly, the US dollar acts as the world’s reserve currency, removing the hassle of exchanging between fiat currencies when conducting international commodities trade.

Both are instances of a currency increasing its adoption by alleviating friction in the financial system. When Bitcoin (or any other cryptocurrency asset) can achieve this, then the institutionalization can begin.

Hunter concedes it is certainly possible to find the friction within the global financial system for a cryptocurrency asset to alleviate. The global payments market is a solid candidate, as individuals currently pay high fees to transact.

“If a crypto could achieve enough stability of value to be used for this purpose, it could eliminate the need to have bank accounts in multiple countries and could allow individuals to transfer money to anyone without paying wire fees,” says Hunter. “If a fully equipped crypto that has a stable value becomes easier and less expensive to transact than a government-issued fiat currency, it could be an innovation that becomes ubiquitous in the global financial services system.”

Sound familiar? ( Hint: think stablecoins , digital fiat !)

It’s all about trust

The larger KPMG report outlines major barriers for facing cryptocurrencies before being institutionalized. Most of them relate adhering to regulatory obligations and keeping up-to-date financial records, which in turn makes the greater finance industry more comfortable with dealing with crypto-assets.

So, to pander to the fatcats, KPMG suggests those who are launching crypto-assets with intent to be adopted by the traditional finance industry should impose strict Know-Your-Customer (KYC) and Anti-Money-Laundering rules on customers and the digital assets they trade.

This includes making use of services that specialize in proving the provenance of digital assets, which can help alleviate concerns of being exposed to illegal activity like money laundering .

Indeed, many cryptocurrency products and services have already bent over backwards for institutionalization , facing immediate, widespread backlash .

It is yet to be seen if any of these measures have helped spur adoption.

Exchange operators and other fintech businesses also need to define clear tax guidelines for investors related to the various kinds of crypto-assets they offer, and must be wary of the rules and regulations surrounding the exchange of crypto-assets classified as securities.

This includes setting protocol for when blockchains undergo hard forks and split into two separate cryptocurrencies, as this presents taxable events that have greater implications for the future of the underlying digital asset being forked.

KPMG’s guide to the institutionalization of cryptocurrencies may very well be handy for the digital assets vying for adoption by the traditional finance world.

However, if Bitcoin’s identity as a real currency relies on being adopted by the very financial system it was built to rebuke, I think we may have found the true fool’s errand.

End of year crypto roundup: How did IOTA perform in 2018?

At a time when cryptocurrency was synonymous with blockchain technology, IOTA proposed a modification.

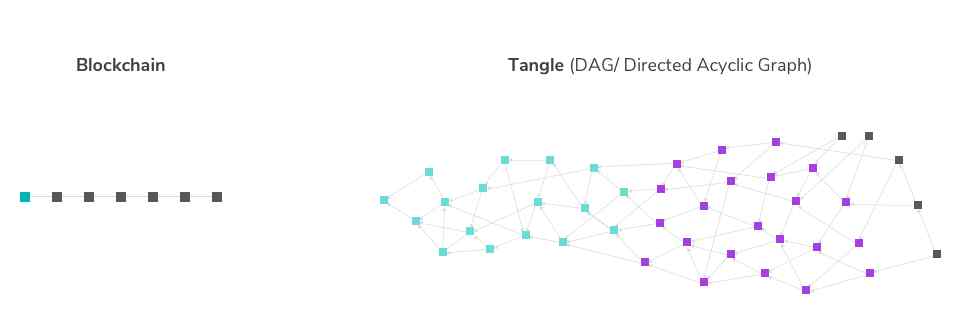

IOTA, as its name would suggest, aspired to be a cryptocurrency for the future of Internet of Things (IoT). But its founders thought that the blockchain had “too sluggish transaction times and skyrocketing fees” to be able to power the world of connected devices. Instead, they introduced a new distributed ledger technology based on Directed Acyclic Graph (DAG) — and named it Tangle.

As a participant, when you want to make a transaction on Tangle, you need to pick two previous transactions at random, validate them, and then connect them with your own transaction. The reward for doing so would be getting your own transaction verified by subsequent participants. This means that unlike with most cryptocurrencies, IOTA transactions don’t incur any fee.

So, what is holding IOTA back from dominating the cryptocurrency market? In order for Tangle to work as intended, IOTA first needs to scale — and so far, it hasn’t.

Additional concerns have been raised about IOTA by many industry experts. MIT’s Digital Currency Initiative (DCI) Director Neha Narula pointed out several cryptography vulnerabilities with Tangle. Ethereum developer Nick Johnson called IOTA a “bad actor” in the open-source community, claiming that it disregards cryptographic best-practices. Critics have also continuously argued that IOTA is actually centralized.

MIOTA/USD performance review

MIOTA, IOTA’s native cryptocurrency, opened the year 2018 at $ 3.56 — a nearly 500 percent increase in price since it first began trading in June last year. Most of this growth was accumulated in November-December during the “crypto boom.”

MIOTA traded above $3.50 for much of the first half of January, but then saw a sharp decline — falling by 25 percent on January 16 from $3.47 to $2.60. By February 1, it was trading at less than $2.

MIOTA market saw a minor upswing in mid-February trading at above $2 again, but saw a quick correction between February 21-23, bringing its price down to $1.60 again.

Starting mid-April, MIOTA’s price rallied upwards hitting $ 2.58 on May 04, when the bull run broke. By May 11, MIOTA was again trading under $2 at $1.86 — a 28 percent drop over the week.

MIOTA maintained a dominant downward trend for the second half of the year. The cryptocurrency was trading at less than a dollar by June end. By August 15, MIOTA was trading at $ 0.45 — a 87 percent drop in market price since the beginning of the year.

From mid-August onwards, MIOTA maintained relative stability in price for the rest of the year, although seeing a slump in November. As of December last week, MIOTA is trading at $0.32. The cryptocurrency has seen a 91 percent drop in market price through 2018, and has lost nearly half of its price from the day it first traded in June 2017.

MIOTA has also performed poorly against BTC in 2018 with the MIOTA/BTC pair losing 64 percent of its value through the year.

IOTA — Major events in 2018

In February, the government of Taipei — Taiwan’s capital — announced that it is working with IOTA for its digital citizen identification project.

The United Nations Office for Project Services (UNOPS) also teamed up with IOTA in April to see how its decentralized ledger technology, Tangle, could help the organization streamline its operations.

In April, IOTA in partnership with IT services company DXC Technology presented a ‘juice-bar robot’ at Hannover-Messe-Industrie trade fair — showing Tangle’s integration for secure digital transformation services. Later that month University College London (UCL) severed its ties with IOTA Foundation on their open security research project. IOTA was also struck with multiple controversies related to internal strifes between team members.

In November, IOTA Foundation announced a partnership with Ledger to integrate its MIOTA tokens with the company’s hardware wallets. The foundation also announced the creation of a new research council to support the IOTA project.

In December, the organization partnered with cybersecurity firm Cybercrypt to create a new hash function called Troika — declaring a $220,000 bounty for anyone who helps find flaws with its security system.

What to expect in 2019

In the last one and a half years, few cryptocurrencies have courted nearly as many controversies as IOTA. Whether it is partnerships gone sour, internal strifes, or technology criticism. In spite of all this, IOTA has managed to remain one of the top performing coins throughout.

A lot of IOTA’s future depends upon whether it can successfully prove critics wrong on the feasibility of Tangle in enabling actual real-time transactions in a time and cost efficient manner as it promises, without compromising on the cryptographic principles.

The market price movements of IOTA show great reliance on overall cryptocurrency sentiments rather than individual performance. While this is true for most cryptocurrencies — the trend is comparatively stronger in case of IOTA.

IOTA is also one of the few top cryptocurrencies that are trading at a lower price at the end of 2018 than when it launched first, which is not true for its contemporaries like Binance Coin (BNB) and NEO (NEO).

The year 2019 could prove to be a ‘make it’ or ‘break it’ year for IOTA — possibly making it one of the more volatile investment options in cryptocurrencies.

Now that you have actionable information on the future of IOTA , it’s time to start investing. With eToro , a leading social trading platform, you can trade manually or copy the actions taken by leading traders, taking much of the stress and work out of your investments.

Facebook is launching a ‘global’ cryptocurrency in 2020 – we’re all doomed

Rumors that Facebook has been working on a cryptocurrency haven’t exactly flown under the radar. And with the latest revelation, the Facebook cryptocurrency machine looks set to step up a gear.

Facebook says it will be launching its cryptocurrency – GlobalCoin – “in about a dozen countries” by the first quarter of 2020. We can expect more solid details by summer, BBC reports .

Over the last few months, Zuckerberg has met with Bank of England governor Mark Carney to discuss the company’s cryptocurrency plans. Zuck also met with representatives from Gemini – a firm founded by institutional crypto-bigwigs and his nemeses, the Winklevoss twins – the Financial Times reports .

How will “GlobalCoin” work?

According to BBC, Facebook wants to make a digital currency that people without a conventional bank account can still use.

The Big F wants to work with banks and brokers to let users convert fiat currencies into its GlobalCoins. The social media firm is allegedly also in talks with money transfer services like Western Union to look for cheap ways to send money abroad.

BBC also says Facebook is in talks with online merchants to accept GlobalCoins as payment, with lower transaction fees as an incentive to use the digital coin.

It all sounds simple enough but there are some big questions that need to be answered.

For one, how decentralized will this system be? (after all, decentralization and censorship-resistance are two of cryptocurrencies’ unique selling points). For two, how is Facebook going to use cryptography to secure users’ assets? For three, who is going to be able to see a person’s transaction history? For four, who is going to control this system? Need I go on?

Earlier this year, JP Morgan took headlines after it announced the first successful use of its digital token, JPM Coin. Naturally, a flurry of reports followed saying that each token is redeemable for fiat, and that the system was powered by blockchain. JPM Coin sounded like a cryptocurrency, with one important distinction: it really isn’t.

JPM Coin is only available for certain institutional investors, and runs on an entirely private and permissioned ( read: centralized ) blockchain.

It’s not outside the realm of possibility that Facebook would follow a similar principle. Proof-of-Work blockchains, like Bitcoin, have long suffered scalability problems , an easy fix for this is to institutionalize the blockchain and centralize its consensus mechanism.

In other words, to ensure GlobalCoins transfer faster than current payment systems, it won’t be that surprising if Facebook takes control and verifies transactions itself.

Ultimately, it means the platform can set the terms of use and decide how people use the virtual asset. If users don’t comply, they could risk having their accounts frozen – and considering the company’s recent deplatforming moves , this is certainly a legitimate threat.

We’ll have to wait and see how strict the terms will be, though.

The end is nigh?

I shouldn’t have to paint the picture, it should be obvious enough, but Facebook’s digital currency will likely give the company another avenue through which it can track its users .

Imagine a bank that not only knows about every financial transaction you’ve made, but also knows your political leaning, your interests, where and with whom you spend your time, and so on.

In some ways, Facebook’s GlobalCoin fits hand in hand with dystopian narratives where the world has come to be dominated by a just few global superpowers. Where each has its own language, its own politic, its own currency, and ultimate control over its citizens – and anyone that doesn’t fit this mold is simply… dealt with.

Hopefully that won’t happen, but given the social media giant’s history of data harvesting and how it has been used to infringe on democracy , we should tread cautiously before making Facebook our bank.

The most terrifying thing about all this, though, is that my mother heard about the news before I did. If my personal history is anything to go by, when this happens, it means the end is probably near.

{kind=link}